New York has long been recognized as an international center of finance and culture, and one of its most defining features is its diversely structured real estate market. In particular, the 421a Tax Abatement program—often encountered through promotional slogans like “Tax Abated Condo”—frequently captures the attention of prospective investors. Against what background did this tax exemption program begin, and what are its benefits and limitations?

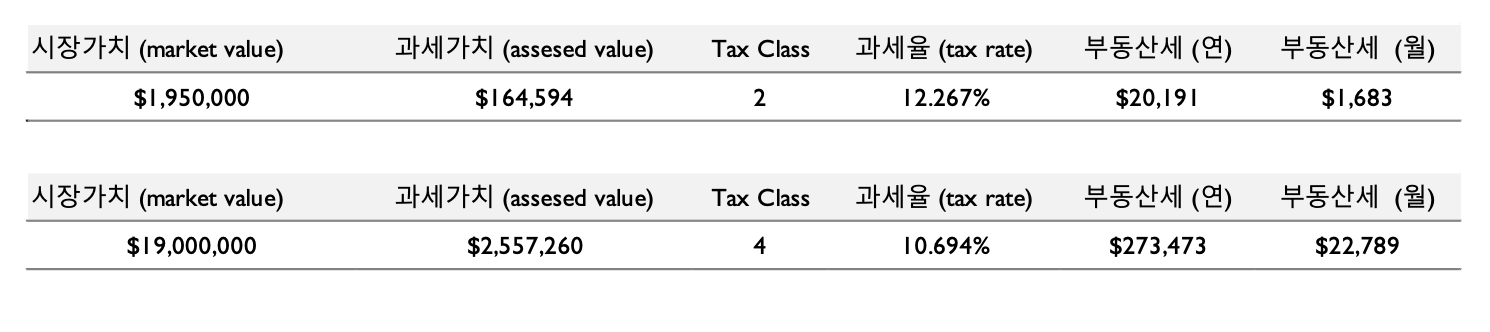

Unlike in South Korea, the United States requires the payment of Property Tax on any owned real estate, regardless of whether it is residential or commercial. This amount is quite substantial; for instance, owning a $2 million condo in Manhattan can result in an annual property tax bill ranging from $20,000 to $25,000.

♦ Residential Condo Property Tax – Based on a Midtown 2-bedroom condo unit (approx. 1,032 sq. ft.)

♦ Commercial Building Property Tax – Based on a Downtown 4-story building (approx. 30,000 sq. ft.)

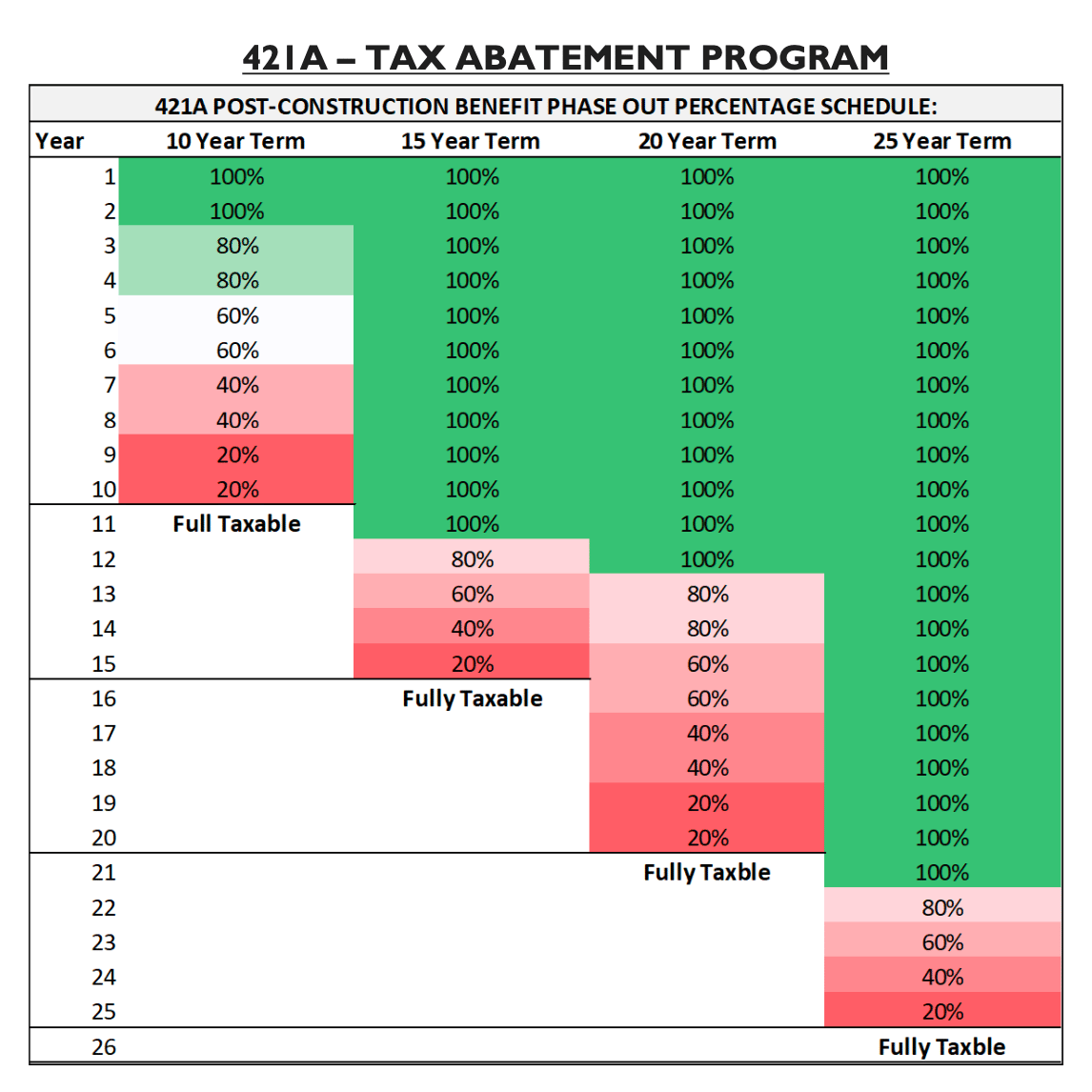

However, in New York, there is a program that provides exemptions from this property tax for as long as 25 years. Known as the 421a Tax Abatement, it offers a very enticing advantage from an investor's perspective. As shown in the accompanying chart, the program provides a period of 100% property tax exemption for 10 to 25 years after the building's completion, with the payment ratio gradually increasing several years before the exemption period expires.

In 1971, New York City launched the 421a program with the aim of improving and regenerating underdeveloped areas. Since its inception, the program has provided developers with attractive tax reduction benefits, while buyers of newly developed condos have enjoyed tax exemptions lasting from 10 to 25 years.

After experiencing a temporary suspension in 2016, the system was restarted in 2017 under the name "Affordable New York," continuing to offer tax exemptions to a large number of developers and investors. However, the program officially expired on June 15, 2022. Consequently, New York developers are voicing concerns over the increasing cost burden, which is having a negative impact on the actual supply of housing.

Currently, led by developers, there are growing calls for the system to be revived, citing an expected supply shortage in the future New York condo market. However, a definitive direction for a successor program has yet to be finalized.

Representative condos benefiting from these programs include One Manhattan Square (20-year), 15 Hudson Yards (20-year), Brooklyn Point (25-year), and 10 Riverside Blvd. (20-year).

For owner-occupiers, these tax-abated condos significantly reduce living expenses for a set period. For investors, they provide stable and higher yields during the exemption window. However, when investing in real estate with guaranteed tax benefits, there are several critical factors to consider:

1. The Dual Effect on Future Resale

Price Dynamics at Purchase vs. Sale While tax abatement programs are an attractive benefit for buyers, they also provide developers with a prime opportunity to sell at higher prices. At the initial purchase stage, buyers often view the tax savings as a positive factor and factor it into their decision. However, one must not overlook that these future tax savings are essentially used as a "credit" applied to the current price. This dynamic shifts significantly during the resale process.

Tax Savings Benefit at the Time of Purchase Buyers enjoy tax savings from the exemption and perceive this amount as having a specific "monetary value." This value acts as a factor in determining the purchase price, effectively reducing the perceived burden of the high initial cost.

Complex Judgments at the Time of Resale When it comes time to resell, new buyers approach the deal differently. As the tax exemption period progresses, the remaining benefit decreases, eventually turning into a future economic burden. This is particularly true when the exemption period is nearing its end or phase-out; the new buyer must take on an additional financial burden (full property taxes) that the previous owner never had to pay.

2. Location and Surrounding Development

Buildings eligible for tax benefits are often located in areas that are less developed than expected or in regions undergoing new, large-scale redevelopment. These locational characteristics present several considerations for both investors and residents.

Relatively Lower Locational Value These buildings tend to have a lower locational value compared to "prime" established areas in the city center. It can take a significant amount of time for the surrounding area to fully develop and stabilize, which can result in initial inconvenience or a sense of instability for residents.

Uncertainty in Regional Development For example, if the purchased condo is surrounded by "Affordable Housing" (housing supplied by the government for low-income residents), the surrounding environment may feel vastly different from the high-end nature of the condo itself. This disparity can act as a constraint on the property's appreciation. Furthermore, because areas with a high density of affordable housing are often tied to complex government policies and various social interests, investors need to be cautious and conduct thorough due diligence.